What Affects Your Citi Diamond Preferred Card Credit Limit?

-

Written by

Aja McClanahan

Written by

Aja McClanahan

-

Edited by

Emily Gadd, CCC™

Edited by

Emily Gadd, CCC™

-

Reviewed by

Jasmin Baron, CCC™

Reviewed by

Jasmin Baron, CCC™

When you open a new credit card, your credit limit determines how much you can spend on the card, including new purchases, cash advances and balance transfers.

The Citi® Diamond Preferred® Card, an advertising partner, is among the best balance transfer credit cards and the top low-APR credit cards thanks to its 0% intro APR for 12 months on Purchases and 21 months on Balance Transfers then 16.49% - 27.24% (Variable) APR. But if your assigned credit limit is low, it’ll be harder to maximize your interest savings from these offers.

If you’re interested in applying for the Citi Diamond Preferred Card, here’s what you need to know about getting the credit limit you want.

400+ Credit Cards

Analyzed independently across 50+ data points in 30+ product categories

Reviewed

By a team of credit card experts with an average of 9+ years of experience

Trusted by

More than one million monthly readers seeking unbiased credit card guidance

CardCritics™ editorial team is dedicated to providing unbiased credit card reviews, advice and comprehensive comparisons. Our team of credit card experts uses rigorous data-driven methodologies to evaluate every card feature, fee structure and rewards program. In most instances, our experts are longtime members or holders of the very programs and cards they review, so they have firsthand experience maximizing them. We maintain complete editorial independence — our ratings and recommendations are never influenced by advertiser relationships or affiliate partnerships. You can learn more about our editorial standards, transparent review process and how we make money to understand how we help you make informed financial decisions.

What Is the Citi Diamond Preferred Card Limit?

A credit limit is the maximum amount a card issuer allows you to borrow on a credit card. It represents your card’s total spending capacity, which you can use for purchases, balance transfers or cash advances. Going over this limit could result in declined transactions or additional fees, depending on your issuer’s policy.

Citi does not publish the credit limit for its Diamond Preferred Card, although it does say in the terms and conditions that the limit could be as low as $500. This is because the limit for each cardholder is based on many factors, such as prevailing interest rates, your credit profile, income and more. When you apply for the card, Citi evaluates these factors to decide your initial limit.

However, responsible use and on-time payments can help you qualify for a higher credit limit. Over time, Citi may reassess your account and offer automatic credit limit increases, or you can request an increase based on your financial situation.

Factors Affecting Your Citi Diamond Preferred Card Limit

When you apply for a new credit card, the issuer typically considers several factors to determine whether to approve you and what your credit limit will be. These include:

1. Income

Your income and employment status are significant factors in your credit limit. People with higher incomes and stable employment histories are more likely to be approved for a higher credit limit.

2. Credit Score

Your credit score reflects your overall creditworthiness. A higher credit score suggests responsible borrowing habits, making lenders more likely to offer a higher credit limit.

A key part of your credit score is your utilization ratio, which measures how much of your available credit you have used. If you’re carrying debt on all of your credit cards up to the limit, you have a high utilization ratio. A card issuer may view a high ratio as a lending risk.

3. Credit History

Your credit history shows how consistently you’ve managed repayments over time, and a strong history of on-time payments can positively impact your credit score.

A low utilization ratio, which represents the percentage of available credit you’re using, also boosts your credit score, which could cause issuers to offer you a higher credit limit.

4. Account History

Some issuers might also consider your account history with them, such as how long you’ve been a customer and your payment history on existing accounts. Together, these factors help issuers make informed decisions about your creditworthiness and the appropriate credit limit to offer.

Additionally, if you already have other cards from Citi with substantial credit limits, you may not qualify for a high credit limit on the Diamond Preferred Card. That’s because issuers typically have a maximum amount of credit they’re willing to extend to one individual.

5. Federal Interest Rates

Another thing that could affect your credit limit is the prevailing interest rate. The federal funds rate, which ultimately influences credit card issuers’ interest rates, can also affect how much a card issuer is willing to lend.

When interest rates are high, lenders may be more cautious and offer lower credit limits to reduce risk. On the flip side, during periods with low interest rates, lenders might be more willing to extend higher credit limits due to reduced borrowing costs.

Is It Possible To Increase Your Citi Diamond Preferred Card Credit Limit?

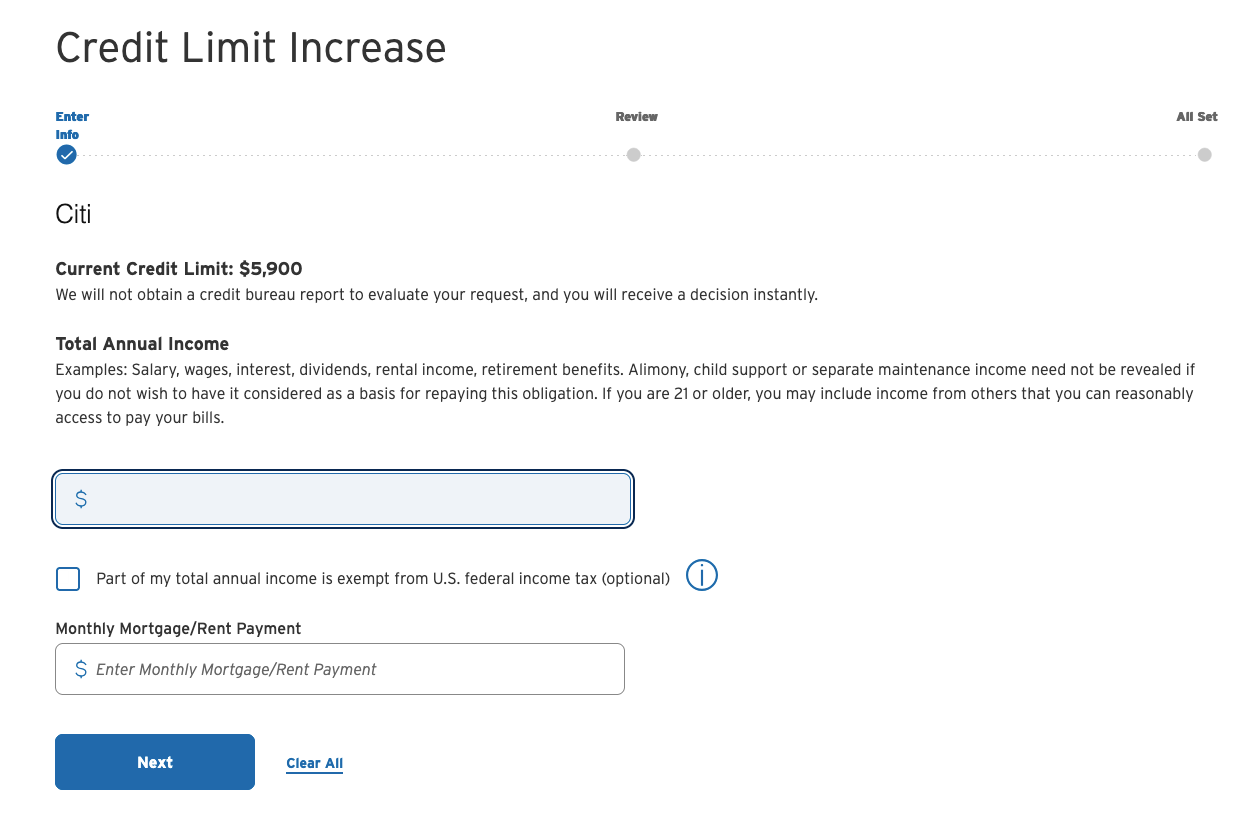

You don’t have to wait for the issuer to review your account and approve a limit increase. The easiest way to request a credit limit increase is to log in to your Citi account online or through the issuer’s mobile app. Navigate to the “Credit Card Services” menu and, under “Card Management,” click on “Request a Credit Limit Increase.” You’ll be asked to update your income and monthly rent/mortgage payment, and once you submit the request, you should receive a decision instantly.

In this example, Citi says it will not perform a credit check when deciding whether to approve your request to increase your credit limit. You should confirm these terms on your own request if you’re concerned about a hard credit inquiry.

You can also request an increase by following these steps:

- Contact Citi’s customer service by calling the number on the back of your card

- Explain that you would like to request a credit limit increase

- Provide any information requested by the customer service representative

- If necessary, verbally consent to a hard credit inquiry

If you’re approved, you’ll receive your new credit limit information immediately via mail or in your secure messaging center.

Why Your Citi Diamond Preferred Card Credit Limit Might Be Decreased

A reduction in your Diamond Preferred Card credit limit can occur for several reasons, such as:

- Missed payments

- High debt-to-income ratio

- Inactivity on your account

This decrease can negatively impact your credit score by increasing your credit utilization rate, which is the ratio of credit used to your overall credit limit.

To avoid a credit limit reduction, make payments on time, keep balances low relative to your credit limit, and use the card periodically to demonstrate activity. Additionally, regularly monitoring your credit report can help you identify and address potential issues that might lead to a decrease.

How Your Citi Diamond Preferred Card Credit Limit Affects Your Credit Score

As mentioned, using less than your credit card limit keeps your credit utilization low and can boost your credit score. Conversely, consistently approaching or exceeding your limit can harm your score by increasing your utilization rate. To maintain a good credit score, you should keep your Diamond Preferred Card balance as low as possible — ideally less than 30% of your limit.

Citi Diamond Preferred Card Credit Limit vs. Other Credit Cards

Though credit limits for some Citi credit cards can exceed $50,000, there’s no way to determine exactly how much you’ll receive once you apply for a Citi Diamond Preferred Card.

For those trying to get a handle on their debt by completing a balance transfer or paying off large purchases over time, the Citi Diamond Preferred Card can be very worth it.

- Citi Entertainment for exclusive event tickets

- 24/7 customer service

- Zero liability for unauthorized charges

- Free access to your FICO score

- Citi Flex Pay plans

- Fraud protection

Tips for Managing Your Citi Diamond Preferred Card Credit Limit

Here’s how you can keep your Diamond Preferred Card credit limit at a reasonable, manageable amount while also keeping your credit score strong:

- Set up account alerts to track spending and avoid exceeding your credit limit

- Use Citi’s online tools or mobile app to monitor your account and credit usage

- Check your balance regularly to stay on top of your finances and prevent overspending

Frequently Asked Questions About the Citi Diamond Preferred Card Credit Limit

What is the standard credit limit for the Citi Diamond Preferred Card?

The Citi Diamond Preferred Card credit limit varies based on the cardholder’s creditworthiness, income and other factors. According to Citi, the minimum is $500, but it can go significantly higher for qualified applicants.

Can I request a higher credit limit after my first year with the Citi Diamond Preferred Card?

Yes, you can request a higher credit limit at any time by calling Citi or through your online account. Approval depends on factors like your payment history, credit score and income. A hard credit inquiry may be required.

How long does it take for a credit limit increase to be approved with the Citi Diamond Preferred Card?

In many cases, you’ll be notified of approval or denial immediately. However, it could take a few days or a week.

What happens if I exceed my Citi Diamond Preferred Card credit limit?

If you exceed your credit limit, Citi may decline transactions until your balance is below the limit. Additionally, you could incur fees or see your credit score drop from a higher utilization ratio.

How does the Citi Diamond Preferred Card’s credit limit compare to premium cards?

The Citi Diamond Preferred Card’s credit limit is competitive but tends to start lower than that of premium cards. Higher limits are possible with strong creditworthiness and higher income.